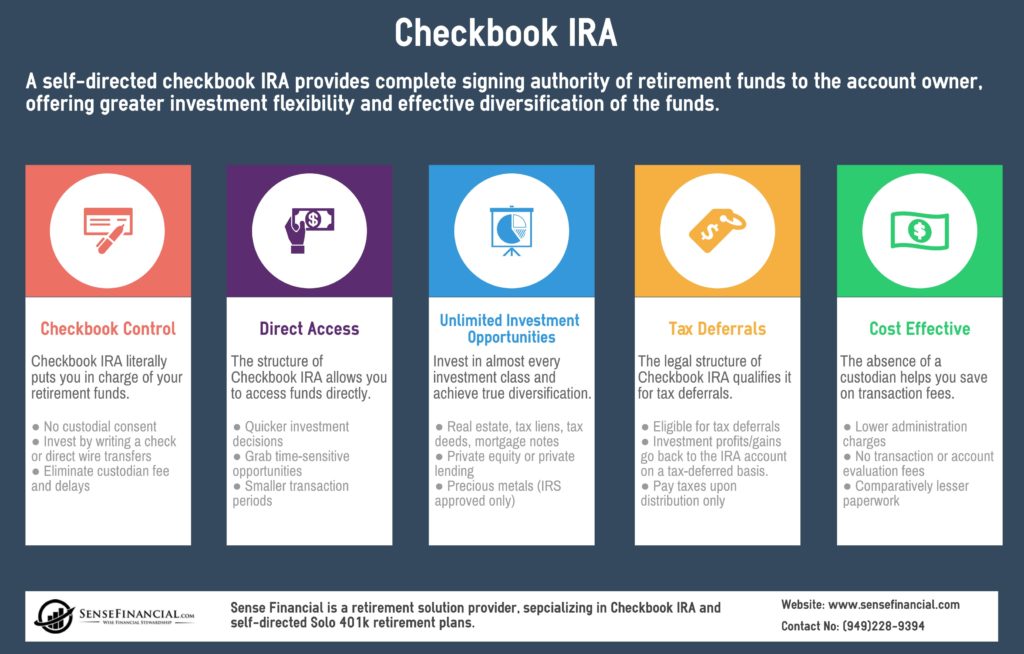

“It’s not how much money you make that makes you rich, it’s how you spend it.” —Charles Jaffe

With a little bit of research, you will find out that the same piece of wisdom has been coined time and again by several financial experts. While there are multiple factors that define as well as affect your financial wellness, we are going to target the most inescapable one – Taxation. When taken at its face value, taxation may appear as inevitable as possible or in the words of Benjamin Franklin, “In this world, nothing can be said to be certain, except death and taxes.”

However, there are some legitimate ways to lower your taxable income, and put that money to work for your future. If you are an owner-only business or highly paid self-employed professional, these strategies could uplift your financial health drastically.

Self-directed Solo 401 k

Solo 401k retirement plans have gathered a huge following over the past couple of years and rightly so. When used efficiently, it could help you increase your retirement savings by up to ten times of the regular IRA contributions.

Self-directed Solo 401 k: What is it?

It is a qualified retirement plan for owner-only businesses and self-employed professionals.

What do you need to know about it?

Contribution limits: Up to $59,000 in 2016 (including catch-up contributions of $6,000 for individuals above 50 years old).

Investment options: Real estate, tax liens, tax deeds, precious metals, private equity, personal financing, and stock/bond investments.

Participant loan: Flexibility to borrow up to 50% of the account balance to a maximum borrowing limit of $50,000.

Four Ways to Cut Your Taxable Income With a Self-Directed Solo 401 k

1. Ten Times Higher Annual Contributions

With an annual contribution limit of up to $59,000, a Solo 401k retirement plan surpasses regular IRA contributions several times. Further, it comprises of two different contribution types, including salary deferral and profit-sharing contributions, allowing you to achieve maximum contributions quickly.

Salary deferral contribution allows you to contribute up to $18,000 in 2016 along with a catch-up contribution of $6,000 for professionals above 50 years.

Profit-sharing contribution allows you to contribute 20 to 25% of your business income to the plan. The total salary deferral and profit sharing contributions are up to $59,000.

2. Deferred Taxation on Capital Gains

Much like its other counterparts, a self-directed Solo 401 k enjoys deferred taxation, allowing your investments to maximize compounding interests. Considering the vast majority of investment options available under self-directed Solo 401k plans, you can boost your wealth generating potential.

The key is to make sure that your Solo 401k provider offers alternative investments. When you invest with a retirement plan, always target long-term gains over short-term growth.

3. Power of Roth Contributions

High-income professionals are often deprived of Roth saving options in regular IRAs but not in a Solo 401k plan. For self-employed professionals, a Roth Solo 401k plan allows after-tax contributions regardless of the income levels. You can contribute up to $24,000 towards your Roth Solo 401k in 2016.

One of the key benefits of establishing a Roth Solo 401k is its ability to offer tax-free earnings. That’s right; all the compound interest generated by your investments goes directly into your account. There are no taxes on qualified withdrawals

4. Purchase Real Estate Under Solo 401k Plan and Forget Rental Income Taxation

If you are a big fan of real estate investing, a Solo 401k plan could introduce you to an entirely new level of profits/returns. Here’s what you need to do.

Purchase a rental property with a positive cash flow through your self-directed Solo 401 k. It’s entirely the same process apart from the fact that your retirement plan will hold the title of the property and all the expenses/profits will go directly from/to the plan.

By doing so, you’ve created an effective income stream, while saving taxes on the rental income. Make sure to:

- Only use a non-recourse loan for the purchase if needed.

- Pay maintenance cost from the plan only.

- Direct rental income to the plan.

In conclusion, we can positively say that a self-directed Solo 401 k allows you to unlock multiple asset options along with a tax-deferred growth of your investments. It is one of the best ways to create a retirement plan that outlasts you.

Image: https://pixabay.com/en/euro-money-finance-piggy-bank-save-870756