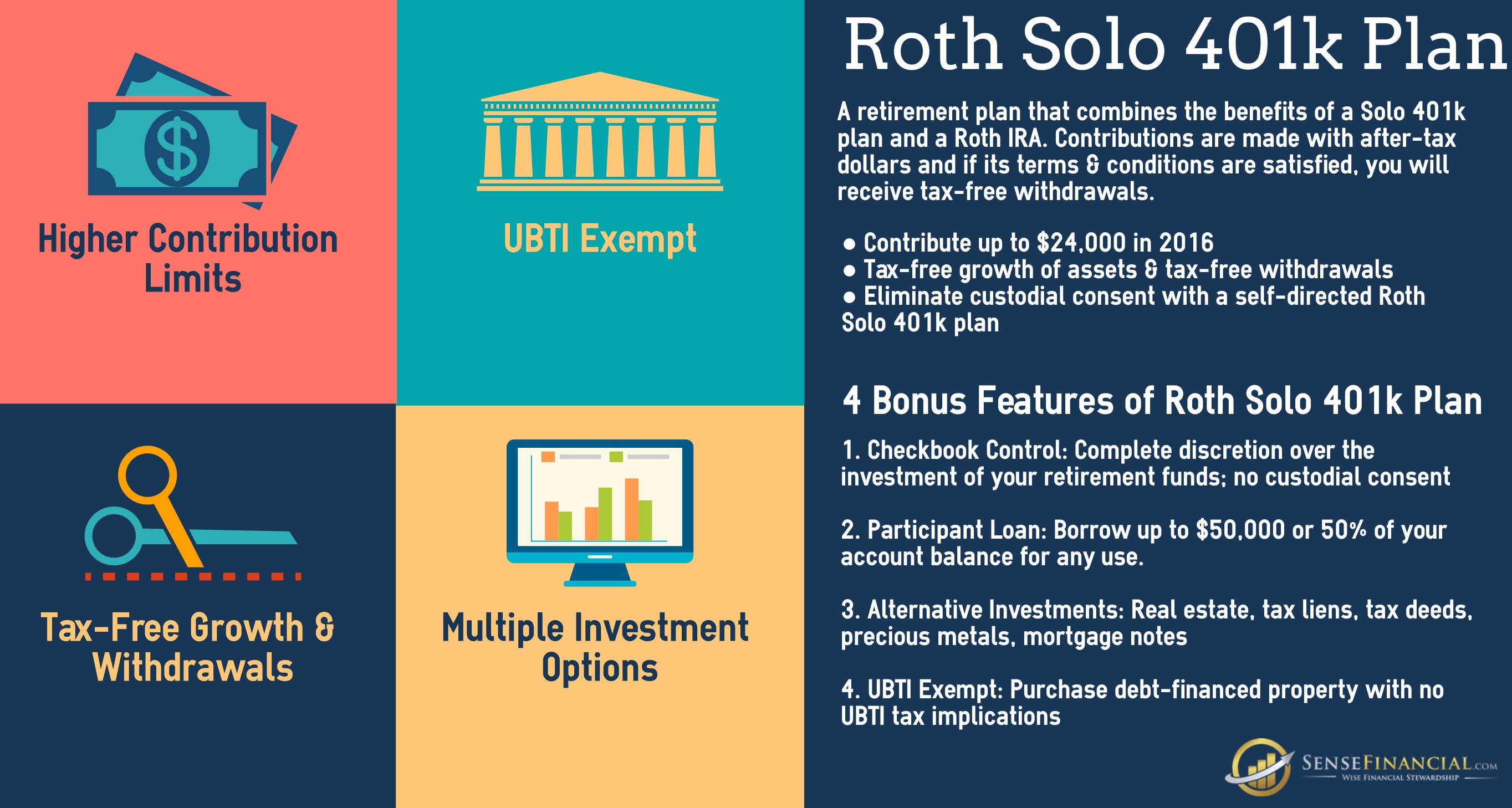

Roth IRA is one of the well-known and oftentimes considered best IRA for self employed. If you are looking for reliable financial investment and retirement account, it is imperative to know more about this plan. Nowadays, you might find it more challenging to decide what retirement account to choose. There is a big difference as well as similarities for 401k vs IRA. Sense Financial Services LLC, the leading provider of premier retirement plan Solo 401k and Self-Directed IRA offers valuable information about these two topmost investment ventures. For Roth IRA, there are essential benefits from this account that you must learn and understand.

Roth IRA is one of the well-known and oftentimes considered best IRA for self employed. If you are looking for reliable financial investment and retirement account, it is imperative to know more about this plan. Nowadays, you might find it more challenging to decide what retirement account to choose. There is a big difference as well as similarities for 401k vs IRA. Sense Financial Services LLC, the leading provider of premier retirement plan Solo 401k and Self-Directed IRA offers valuable information about these two topmost investment ventures. For Roth IRA, there are essential benefits from this account that you must learn and understand.

Roth IRA plan is not subject to Required Minimum Distribution Rules

One of the reasons why Roth IRA is considered the best IRA for self employed is that it is not required to comply with RMD rules unlike traditional retirement accounts. The Required Minimum Distribution rules subject the account holder to pay taxes on distributions. This is a requirement which takes effect as soon as the plan holder reaches 70 ½ years old. If you are not subject to RMD, tax-free income is accumulated, allowing the account to boost its accumulated and tax-free income throughout the duration of the owner’s lifetime.

401k or Best IRA for self employed: Which is best - distribution extension for surviving spouse

Roth IRA is not only the best IRA for self employed account holders but also a lucrative and useful investment for the surviving spouse. That’s because the account beneficiary of the retirement plan can still opt to continue the contribution to the plan. Or the beneficiary could opt to combine this Roth IRA to their own retirement plan, basically the same Roth IRA. This means that the surviving spouse could take over and benefit from the account particularly the growth on investment with its tax-free features. On the other hand, traditional retirement plans are not allowed to be combined and merged into the surviving spouse’s IRA. The beneficiary is also not allowed to opt for an additional contribution to the existing account.

Roth IRA account holders do not pay 10% early distribution withdrawal penalty

Account holders who decide to withdraw their account contribution before they reach the age of 59 ½ are not subject to the 10% payment of the early withdrawal penalty. Account holders could basically withdraw their converted or contributed amounts to their Roth IRA retirement account without the hassle of paying taxes or the penalty as long as they comply with the 5-year wait period making it the best IRA for self employed.